13/05/2019

First quarter trading update

Dignity plc (Dignity, the Company or the Group), the UK's only listed provider of funeral related services, announces its trading update for the first quarter of 2019.

PDF version of the first quarter trading update

| 13 week period ended 29 March 2019 |

13 week period ended 30 March 2018 |

Decrease (per cent) |

|

| Underlying revenue (£million) | 81.1 | 95.1 | 15 |

| Underlying operating profit (£million) | 21.7 | 37.5 | 42 |

| Number of deaths | 159,000 | 181,000 | 12 |

Alternative performance measures

All measures marked as underlying in the table above and throughout this announcement are alternative performance measures. The reasons for the Group's use of alternative performance measures are provided in the section on alternative performance measures at the end of this announcement.

Financial summary

Operating performance in the first quarter was below the Board's expectations as a result of the significantly lower than expected number of deaths. Funeral market share and average income were in line with the Board's expectations. Underlying operating profit by division is summarised in the table below:

| Underlying operating profit by division |

13 weeks ended 29 March 2019 £m |

13 weeks ended 30 March 2018 £m |

| Funeral division | 18.4 | 27.9 |

| Crematoria division | 10.9 | 13.0 |

| Pre-need division | - | 1.5 |

| Central overheads | (7.6) | (4.9) |

| Underlying operating profit | 21.7 | 37.5 |

Number of deaths

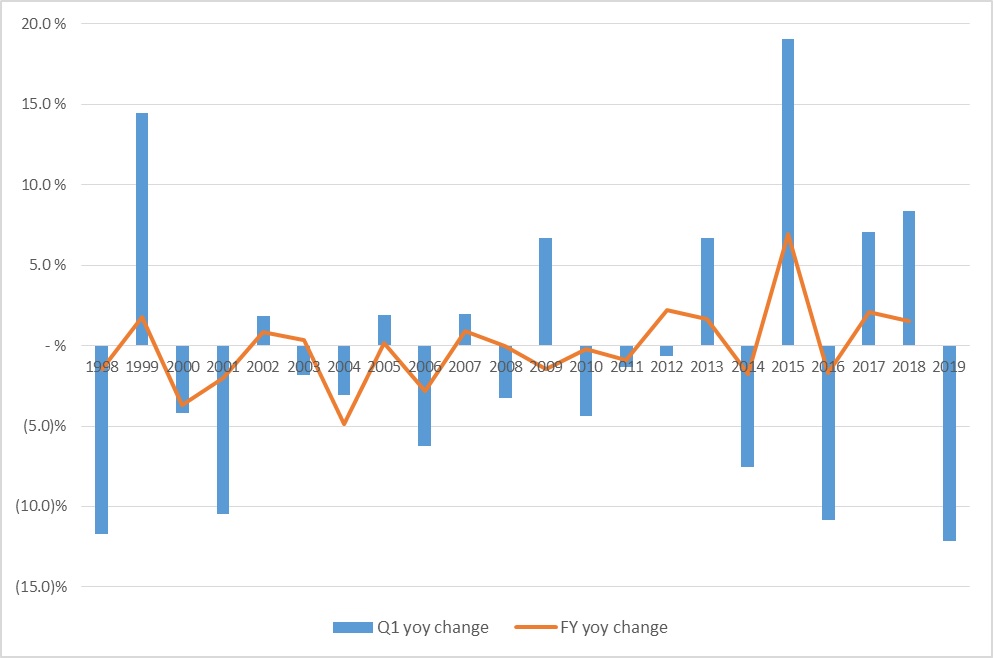

The absolute number of deaths decreased by approximately 12 per cent to 159,000 from 181,000 in the comparative period last year, continuing the low number reported by the Group in its preliminary results presentation for the first nine weeks of 2019. Historical data indicates that it is likely that this proportional decrease will not continue throughout the remainder of the year and that the full year will finish within approximately three per cent of the previous year. A table and chart showing this data is appended to this statement. Longer term expectations, based on the Office for National Statistics ('ONS') forecasts, remain unchanged. The ONS expects long-term increases in the number of deaths, reaching approximately 700,000 per year by 2040.

Funeral operations

Key changes in the profitability of the Group’s funeral business are detailed in the table below:

| Funeral operations | £m |

| Underlying operating profit – Q1 2018 | 27.9 |

| Impact of: | |

| Number of deaths | (6.8) |

| Market share | 0.8 |

| Lower average incomes | (4.0) |

| Reduction in costs | 0.5 |

| Underlying operating profit – Q1 2019 | 18.4 |

Funeral market share

Funeral market share continued to show a positive response to the Group's updated service offering and price points introduced in 2018. The Group performed 19,200 funerals in the first 13 weeks of the year (Q1 2018: 21,400), representing a market share of 12.0 per cent (Q1 2018: 11.7 per cent). On a comparable basis, excluding any volumes from locations not contributing for the whole of 2018 and 2019 to date (and therefore excluding eight locations closed in 2018 and a further three locations closed in the first quarter of 2019), market share was 11.8 per cent compared to 11.6 per cent for the same period in 2018.

Average income

As demonstrated in the table, average income per funeral was approximately £190 lower than the same period in 2018, slightly below the amount expected and previously guided by the Group. The Group continues to expect average income for the remainder of the year to be approximately £2,940 as it continues its trials and plans to implement its tailored funeral nationally.

| Funeral type | FY 2018 Actual |

Q1 2019 Actual |

Q1 2018 Actual |

|

| Average revenue (£) |

Full service | 3,735 | 3,542 | 3,875 |

| Simple and limited service | 2,350 | 2,159 | 2,100 | |

| Pre-need | 1,705 | 1,826 | 1,680 | |

| Other (including Simplicity) | 570 | 773 | 580 | |

| Volume mix (%) |

Full service | 48 | 52 | 55 |

| Simple and limited service | 19 | 14 | 12 | |

| Pre-need | 27 | 27 | 28 | |

| Other (including Simplicity) | 6 | 7 | 5 | |

| Weighted average (£) | 2,734 | 2,691 | 2,883 | |

| Ancillary revenue (£) | 239 | 213 | 212 | |

| Average revenue (£) | 2,973 | 2,904 | 3,095 | |

Crematoria operations

Key changes in the profitability of the Group's crematoria business are detailed in the following table:

| Crematoria operations | £m |

| Underlying operating profit – Q1 2018 | 13.0 |

| Impact of: | |

| Number of deaths | (2.0) |

| Market share | 1.0 |

| Lower average incomes | (0.5) |

| Cost base increases | (0.6) |

| Underlying operating profit – Q1 2019 | 10.9 |

Crematoria performed 18,000 cremations in the period (Q1 2018: 19,100), representing a market share of 11.3 per cent (Q1 2018: 10.6 per cent) for the first quarter of the year. This particularly strong performance is mainly attributed to the increased popularity of direct cremations.

Pre-need accounting

As previously announced, the Group reduced the level of marketing allowances it claimed from the trusts when it made a plan sale with effect from July 2018. As expected, the Group's pre-need division reported no underlying operating profit in the first quarter of 2019.

In addition, the adoption of IFRS 15 in 2019 has resulted in a change to the Group's accounting policies for the sale of trust based pre-arranged funeral plans. The adoption of this standard does not affect the Group's underlying reporting measures. See the section on alternative performance measures at the end of this announcement for further details.

Marketing and digital activity

The Group’s online Funeral Notices service is now fully rolled out and is being used by clients across the country. In the first quarter over half a million consumers have viewed a Funeral Notice and more than £250,000 in charitable donations has been pledged via the online donations facility. The Group has continued to expand its online reach, providing more advice and guidance, which has resulted in a near threefold increase in visits to the Group’s websites compared to the same prior year period.

Transformation Plan update

Activity has continued to accelerate with a focus on:

- Following the finalisation of future efficient branch networks, the commissioning of a development partner to co-ordinate the property investment agenda;

- Ongoing development and monitoring of trials of unbundled services for bespoke funeral arrangements;

- Continued enhancement for clients in the Group’s online digital offering including Funeral Notices and improved site structure and ease of use;

- Formalisation of projects addressing central capability including initiatives focused on the Group’s Client Service Centre, purchase-to-pay cycle and procurement expertise;

- Continued investment in central capabilities particularly Human Resources and Marketing;

- Detailed engagement with front-line colleagues on specific role design and ways of working ahead of testing the Group's future network operating model; and

- Recruitment of an IT Director to lead product selection and enhance the Group's development capabilities.

Competition and Markets Authority investigation

On 28 March 2019, the Competition and Markets Authority ('CMA') confirmed its widely anticipated full market investigation into the funeral and crematoria sector. Dignity welcomes the investigation and is cooperating fully with the CMA's enquiries. In particular, Dignity has established a strong working group of internal and external resource and will seek to focus on these key areas:

- Quality of service provided to meet customer needs;

- Regulation of the industry to protect customers; and

- Capital employed in the crematoria.

The Group will make further announcements as appropriate.

Outlook

The year has started below the Board's expectations primarily as a result of the number of deaths so far in 2019. Achievement of full year expectations will rely heavily on the number of deaths in the remainder of the year compared to 2018. Historical data over the last 20 years indicates that the final volume is likely to be within three per cent of the previous year. If deaths were 580,000 (approximately three per cent lower), then all other matters being equal, underlying operating profits for the full year could be approximately £3 million to £4 million lower than originally anticipated. Clearly, this would require a significant increase in the number of deaths compared to last year in the second half of the year and would result in the financial performance for the year being more heavily weighted towards the second half of the year.

Mike McCollum, Chief Executive of Dignity, commented:

"Our primary focus for 2019 remains the execution of our transformation programme, which seeks to build a more coherent, cohesive and technology-enabled business, geared to meeting the changing needs of our customers, whilst remaining focused on excellent client service. This will deliver our vision to lead the funeral sector in terms of quality, standards and value-for-money.

Whilst the number of deaths in 2019 may mean that our short-term financial performance is lower than we originally anticipated, I am confident that the changes we are making will allow us to generate sustainable growth in the medium to long-term."

For further information please contact:

| Mike McCollum, Chief Executive | |

| Steve Whittern, Finance Director | |

| Dignity plc | +44 (0) 207 466 5000 |

| Richard Oldworth | |

| Chris Lane | |

| Catriona Flint | |

| Buchanan | +44 (0) 207 466 5000 |

| www.buchanan.uk.com | dignity@buchanan.uk.com |

Conference call details

A conference call for analysts and institutional investors will be held at 9.30am (BST) this morning.

UK Toll-Free: 08003589473

UK Toll: +44 3333000804

Participant PIN Code: 23562150#

URL for international dial in numbers: http://events.arkadin.com/ev/docs/NE_W2_TF_Events_International_Access_List.pdf

A recording of this conference call will subsequently be available at http://www.dignityfuneralsplc.co.uk.

Historical number of deaths

Year |

Q1 Number of deaths |

FY Number of deaths |

Q1 Increase/(decrease) (per cent) |

Q1 Increase/(decrease) (per cent) |

| 1997 |

188,000 |

618,000 |

n/a |

n/a |

| 1998 |

166,000 |

609,000 |

(11.7) |

(1.5) |

| 1999 |

190,000 |

620,000 |

14.5 |

1.8 |

| 2000 |

182,000 |

597,000 |

(4.2) |

(3.7) |

| 2001 |

163,000 |

585,000 |

(10.4) |

(2.0) |

| 2002 |

166,000 |

590,000 |

1.8 |

0.9 |

| 2003 |

163,000 |

592,000 |

(1.8) |

0.3 |

| 2004 |

158,000 |

563,000 |

(3.1) |

(4.9) |

| 2005 |

161,000 |

564,000 |

1.9 |

0.2 |

| 2006 |

151,000 |

548,000 |

(6.2) |

(2.8) |

| 2007 |

154,000 |

553,000 |

2.0 |

0.9 |

| 2008 |

149,000 |

553,000 |

(3.2) |

- |

| 2009 |

159,000 |

545,000 |

6.7 |

(1.4) |

| 2010 |

152,000 |

544,000 |

(4.4) |

(0.2) |

| 2011 |

150,000 |

539,000 |

(1.3) |

(0.9) |

| 2012 |

149,000 |

551,000 |

(0.7) |

2.2 |

| 2013 |

159,000 |

560,000 |

6.7 |

1.6 |

| 2014 |

147,000 |

550,000 |

(7.5) |

(1.8) |

| 2015 |

175,000 |

588,000 |

19.0 |

6.9 |

| 2016 |

156,000 |

578,000 |

(10.9) |

(1.7) |

| 2017 |

167,000 |

590,000 |

7.1 |

2.1 |

| 2018 |

181,000 |

599,000 |

8.4 |

1.5 |

1998, 2004, 2010 and 2016 have been adjusted to allow for the fact these were 53 week years.

Alternative performance measures

The Board believes that whilst statutory reporting measures provide a useful indication of the financial performance of the Group, additional insight is gained by excluding non-underlying items which comprise certain non-recurring or non-trading transactions.

Non-underlying items

The Group's underlying measures of profitability exclude:

- amortisation of acquisition related intangibles;

- external transaction costs;

- profit or loss on sale of fixed assets;

- Transformation Plan costs (see below);

- operating and competition review costs;

- one-off costs in respect of the defined benefit pension obligations;

- trade name write-off and impairments;

- profit or loss of associates;

- the impact of IFRS 15; and

- the taxation impact of the above items together with the impact of taxation rate changes.

Non-underlying items have been adjusted for in determining underlying measures of profitability as these underlying measures are those used in the day-to-day management of the business and allow for greater comparability across periods.

Transformation Plan costs

Given the on-going transformation of the Group’s business will result in significant, directly attributable non-recurring costs over the period of the Transformation Plan, these amounts are excluded from the Group’s underlying profit measures and treated as a non-underlying item.

These costs will include, but are not limited to:

- external advisers’ fees;

- directly attributable internal costs, including staff costs wholly related to the Transformation (such as the Transformation Director and project management office);

- costs relating to any property openings, closures or relocations;

- rebranding costs;

- speculative marketing costs; and

- redundancy costs.

Calculation of underlying reporting measures

Underlying profit measures (including divisional measures) are calculated as profit before non-underlying items.

Underlying earnings per share is calculated as profit after taxation, before non-underlying items (net of tax), divided by the weighted average number of Ordinary Shares in issue in the period.

Underlying cash generated from operations excludes non-underlying items on a cash paid basis.

Like-for-like annualised operating profit ('LFL annualised operating profit')

The Group recognises that its current measure of underlying operating profit and statutory measures of financial performance will not provide a transparent view of financial performance whilst the Group’s Transformation Plan is being implemented. This is because such existing measures will not give clarity of the economic impact of changes made part way through the period (e.g. new investments, location closures and staff changes). The Group therefore plans to introduce an additional alternative performance measure for the period of the Transformation Plan.

LFL annualised operating profit will adjust underlying operating profit in such a way as to reflect a best estimate of the Group’s sustainable profitability into the following year. An explanation of the changes to underlying operating profit in arriving at LFL annualised operating profit will be provided in each reporting period.

As there have not been any significant changes in locations or staffing in 2018 or the first quarter of 2019, LFL annualised operating profit is considered to be the same as underlying operating profit for the periods reported.

Forward-looking statements

This announcement and the Dignity plc investor website may contain certain 'forward-looking statements' with respect to Dignity plc ("the Company") and the Group’s financial condition, results of its operations and business, and certain plans, strategy, objectives, goals and expectations with respect to these items and the economies and markets in which the Group operates.

Forward-looking statements are sometimes, but not always, identified by their use of a date in the future or such words as 'anticipates', 'aims', 'due', 'could', 'may', 'should', 'will', 'would', 'expects', 'believes', 'intends', 'plans', 'targets', 'goal' or 'estimates' or, in each case, their negative or other variations or comparable terminology. Forward-looking statements are not guarantees of future performance. By their very nature forward-looking statements are inherently unpredictable, speculative and involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. Many of these assumptions, risks and uncertainties relate to factors that are beyond the Group’s ability to control or estimate precisely. There are a number of such factors that could cause actual results and developments to differ materially from those expressed or implied by these forward-looking statements. These factors include, but are not limited to, changes in the economies and markets in which the Group operates; changes in the legal, regulatory and competition frameworks in which the Group operates; changes in the markets from which the Group raises finance; the impact of legal or other proceedings against or which affect the Group; changes in accounting practices and interpretation of accounting standards under IFRS, and changes in interest and exchange rates.

Any forward-looking statements made in this announcement or the Dignity plc investor website, or made subsequently, which are attributable to the Company or any other member of the Group, or persons acting on their behalf, are expressly qualified in their entirety by the factors referred to above. Each forward-looking statement speaks only as of the date it is made. Except as required by its legal or statutory obligations, the Company does not intend to update any forward-looking statements.

Nothing in this announcement or on the Dignity plc investor website should be construed as a profit forecast or an invitation to deal in the securities of the Company.

Other information

Dignity (2002) Limited (the holding company of those companies subject to the securitisation) has today issued reports to the Rating Agencies (Fitch and Standard & Poor's), the Security Trustee and the holders of the Secured Notes issued in October 2014 in connection with the securitisation.

Copies of these reports are available at http://www.dignityfuneralsplc.co.uk.